A mutual offset (also called a set-off of debts) is used when two companies act as both supplier and customer to each other. For example, Company A sells goods to Company B, and at the same time buys materials or services from Company B. As a result, both parties have receivables and payables with each other.

To simplify settlements, the companies can agree to offset the mutual debts. The procedure usually involves drawing up a mutual offset (set-off) statement or agreement, which confirms the amount of reciprocal obligations being canceled.

In accounting records, each company reduces both the accounts receivable and accounts payable by the offset amount. Only the remaining balance (if any) is paid in cash or settled separately.

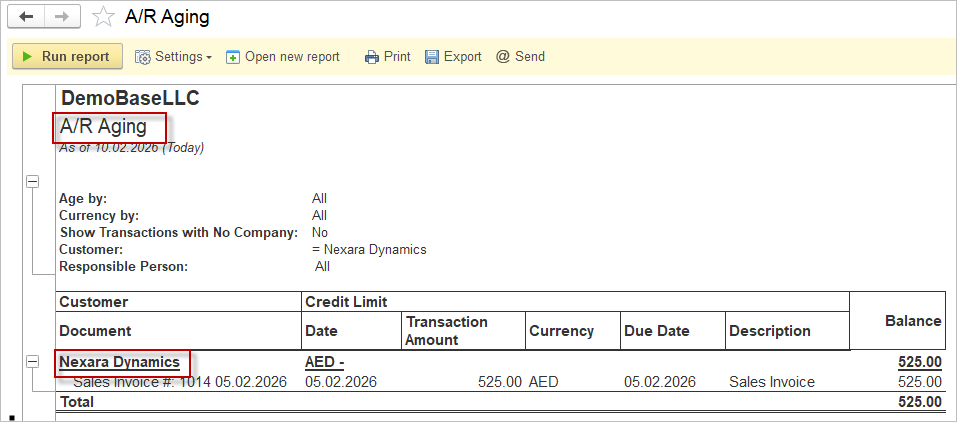

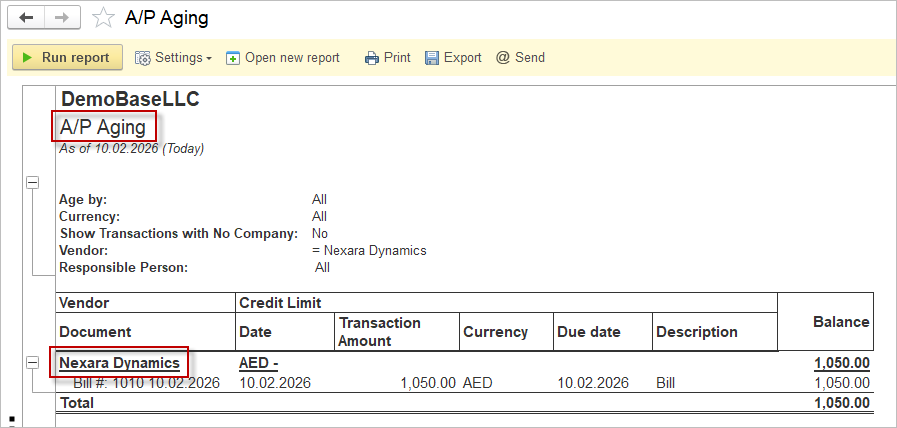

Step 1. Verify the balances

Both parties review:

- outstanding receivables (invoices issued),

- outstanding payables (invoices received), and confirm that all obligations are undisputed and overdue or maturing according to the contract.

Step 2 Draft a mutual set‑off agreement or statement

The agreement should specify:

- the parties,

- the base invoices or contracts,

- the amounts to be offset,

- the date of the set‑off,

- any reference to tax or legal requirements in the relevant jurisdiction.

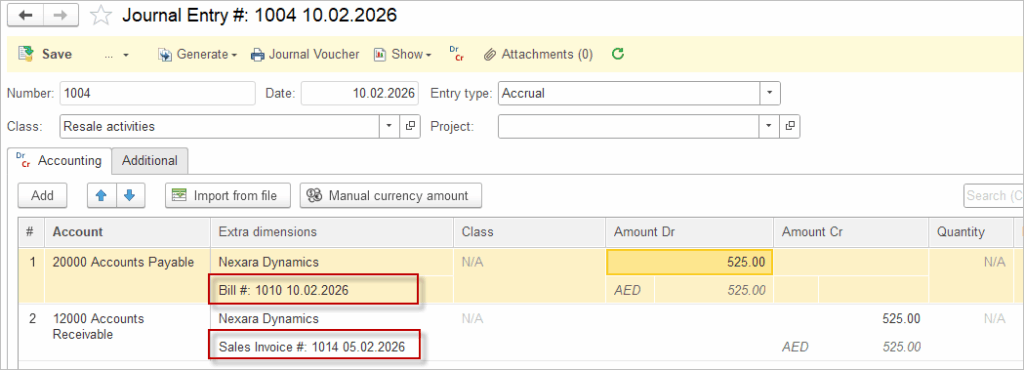

Step 3. Make accounting entries with a Journal entry.

The offset is reflected by reducing both accounts receivable and accounts payable by the same amount. It is crucial to enter the Documents as an Extra Dimension.

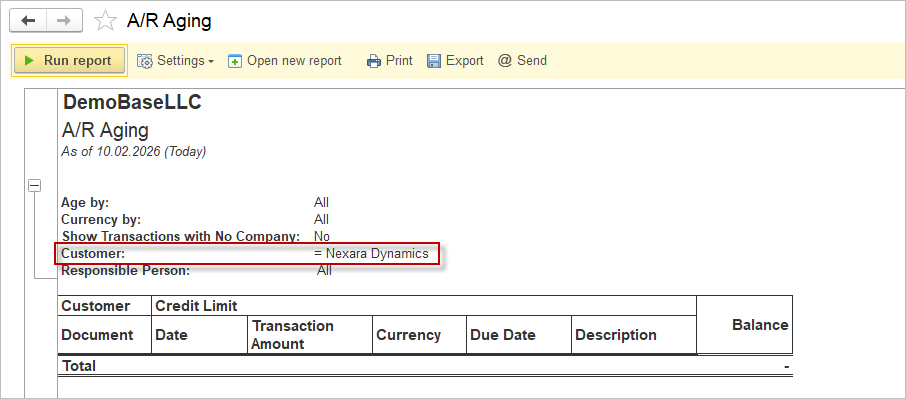

Step 4. Run a customer statement or aged receivables report for the counterparty and confirm that the offset document appears as an applied credit or deduction against the original invoice.

Please note: VAT remains due on full supply values

Even after offset, both parties must account for VAT on the full invoice amounts (not the net balance).

Mutual set-off tax treatment varies significantly by jurisdiction. Always consult a qualified local tax professional or advisor to ensure compliance with applicable laws and regulations before implementing any set-off transactions.