Profit margin scheme VAT is a special way of calculating VAT where tax is charged only on the profit margin, not on the full selling price of the goods.

Concept and scope #

- Under a profit margin scheme, VAT is calculated on the difference between the purchase price and the selling price of eligible goods, and this margin is treated as inclusive of VAT.

- The scheme usually applies to specific categories such as second‑hand goods, antiques, works of art and similar items purchased without deductible input VAT.

Required Settings #

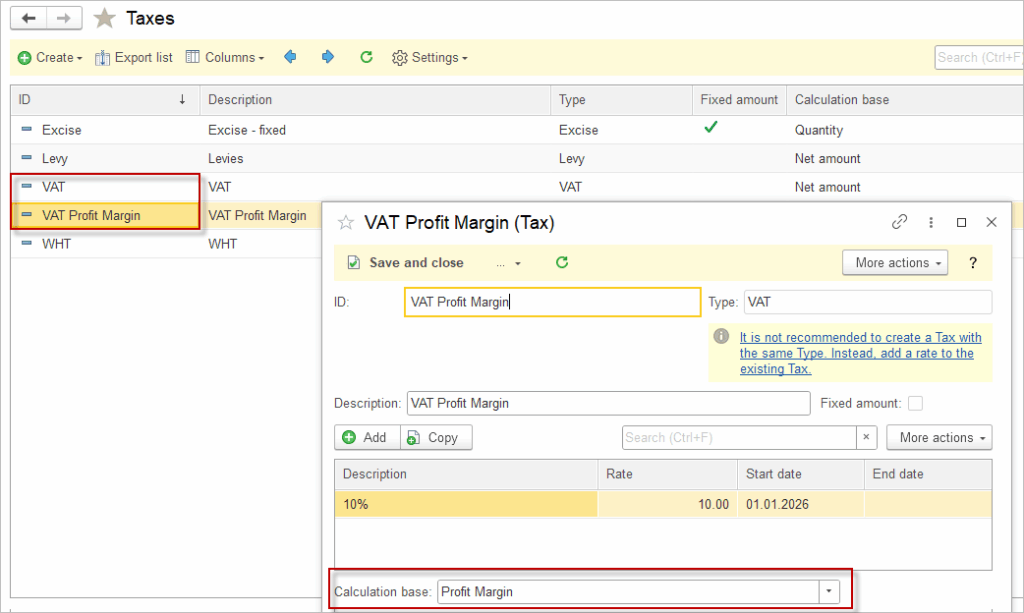

- Create a new Tax with VAT Type and specify the Calculation base as Profit margin.

- Create the applicable tax rate and include them into a Tax group that will be assigned to Items and Companies.

Document processing #

- Sales documents using the profit margin scheme must suppress a separate VAT amount on the customer invoice and show only the gross selling price, while VAT is calculated and stored internally.

Accounting and reporting #

- For general ledger posting, the system should split the margin into VAT and net revenue: debit customer, credit revenue (net of VAT), credit VAT payable based on the VAT fraction of the margin.

- The software must be able to produce VAT return reports that aggregate profit‑margin scheme sales separately from normal VAT supplies, showing total margin, taxable base, and VAT due for the period.

Audit trail and controls #

- To comply with tax authority requirements, the system should maintain item‑level audit trails including purchase documents, sales documents, margin calculation, and stock movement history for goods sold under the scheme

- Access controls and validation rules are recommended so that only authorised users can assign the profit margin scheme to items or documents, reducing the risk of misuse and tax penalties.