The company purchases a passenger car for business use, registered as a personal vehicle rather than a goods vehicle. According to local VAT regulations, VAT on passenger cars is non-deductible.

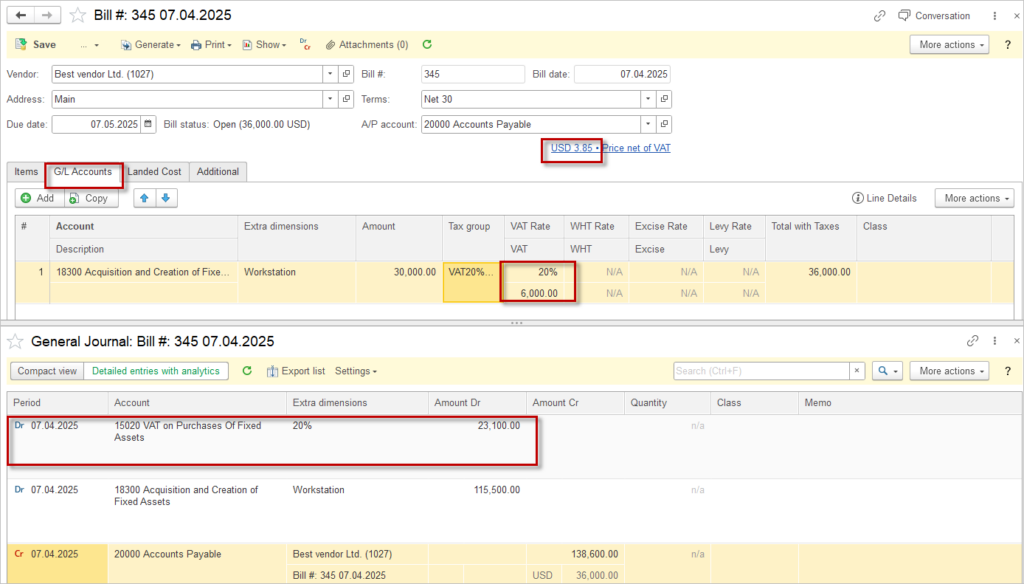

Step 1 is to book the Bill for car purchase.

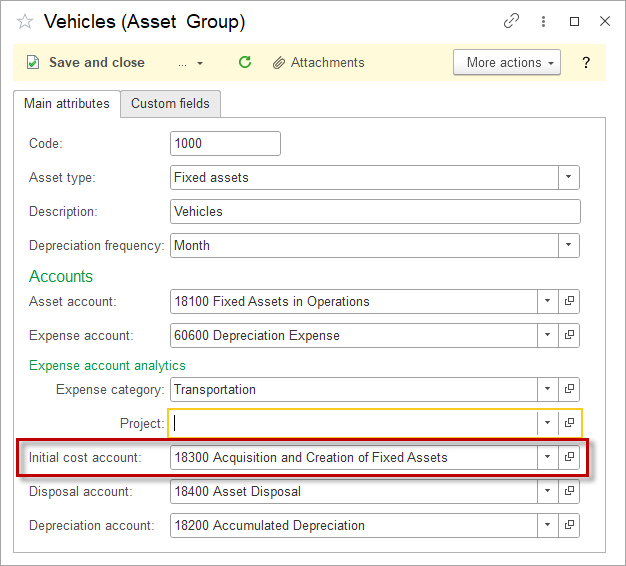

On the G/L tab, select the appropriate account which is set as Initial cost account in the Asset group where the acquired asset belongs.

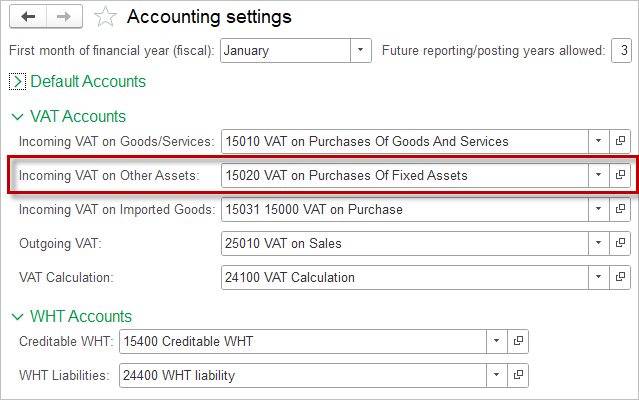

Input VAT shall be booked to the G/L account Incoming VAT on other assets set in Accounting settings.

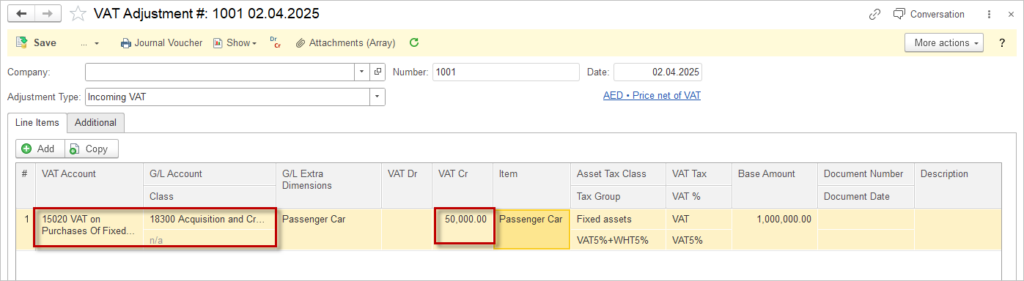

Step 2 VAT amount has to be transferred from the input VAT account. Since the VAT cannot be deducted, it must be recorded as part of the cost of acquiring the asset. This is made by the VAT Adjustment document. Adjustment type is set to Incoming VAT, amount entered in the Cr column, as the aim to credit the VAT account.

Important:

In this case it is assumed, that no Tax invoice has been posted for the purchase Bill. A Tax invoice would have transferred the VAT amount to the VAT calculation account, where the VAT amounts are collected until claimed.

If where would have been a Tax invoice posted, the VAT adjustment document would have the Adjustment type VAT calculation and would credit the VAT calculation account.

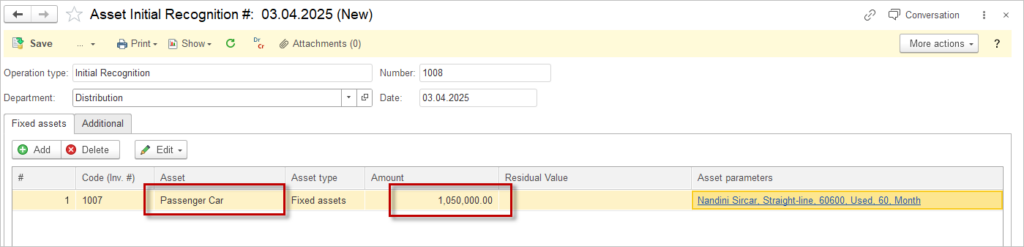

Step 3 is to book the initial recognition of the asset in the amount including the VAT. Depreciation calculations will include the VAT component since it forms part of the asset’s acquisition cost.